Americans have been taught by banks and real estate agents that their home is a great asset. That is true, but it is their asset, not yours.

As a once licenced Realtor, who currently owns three investment properties, I am a believer in homeownership, but NOT all home ownership. In most situations, homeownership is a great investment for everyone but the homeowner.

In 2008, Americans were shocked when banks booted them from “their” cozy homes. They felt cheated and robbed, and many blamed the banks.

Yet, the banks are doing exactly what banks have always done: lend money for profit.

In fact, we might be grateful that there are such people willing to loan us money. The problem is that most Americans are lacking the education to borrow money. Having entrusted our education to the government, Americans are clueless when it comes to real property.

We walk into our banks like little guppies in a shark tank, and are shocked when the sharks swallow us up.

Well, after you finish reading this post, you will never be “taken” again. You will have a better understanding of real estate than 99% of Americans, including many real estate agents!

The Truth About Homeownership

Let’s start at the beginning.

1. You are NOT a homeowner:

Do you own a home? No, it isn’t likely.

Unless you paid cash, you really just own a huge debt. And when I say huge, I mean ginormous!

Think you just bought a 200,000 house? At an 8% interest rate (a great rate before the 2008 housing crash) over 30 years, you really bought a $528,310 house.

2. Amortization Means You’re NOT Buying Down Your Home:

Interest is amortized, or front-loaded. Amortization means that you aren’t buying your house, or at least not anytime soon.

For the first five years, nearly all of your monthly payment goes straight to interest. It isn’t until the last ten years that the tide shifts and your payment really starts to eat down the principle.

Since the average American moves on average once every 5 years, most “homeowners” only ever pay banks interest!

3. You are a low-risk Tenant:

The reason banks are so set on calling you a “homeowner”, is that tenants who think they are homeowners are ideal renters.

They are more likely to maintain the property and invest money into the house. This also makes home-owning tenants less likely to default on their rent (mortgage) because they don’t want to lose “their” home.

4. You Move Too Much to Own:

The average person moves 10 times as adults, nearly once every 5 years. Everytime you buy a new home you pay closing costs, approximately 2-5% of the purchase price.

Let’s say that you buy 10 homes in your lifetime for $200,000 with 3.5% in closing costs. You have now shelled out $70,000 just in closing fees. But we are just getting warmed up.

10 moves also means 10 real estate commissions! With our same $200,000 homes that is $120,000 in realtor fees over your lifetime!

5. Real Estate Agents are Salesmen:

Never ask your real estate agent if it is a good time to buy and expect him to say anything but yes! He is a salesman; it is always a good time to buy!

When I bought my first house, just months before the great crash of 2008, my real estate salesman assured me that there was never a better time to buy! That property is now a rental that plagues me to this day and is just now beginning to bob its chimney above water.

6. You Don’t Want Property Values to Go Up:

A few months ago, voters in Meridian Idaho did something monumental, they voted down one of the school’s excessive property levies.

Teachers went crazy on the internet calling homeowners stupid. Didn’t we know that more money means better schools and better schools means increased property values?

I couldn’t help myself. I got into a Facebook spat because, in most cases, the worst thing that can happen to a property owner is his home’s market value goes up! As property values go up, so do taxes!

So, not only would we have to pay the school levy, but we’d have to pay more in taxes on the increased value. And it’s even worse when we go to sell!

Let me explain. It is simple math that every adult should understand; thank heavens we got a pre-Common Core education, right?

Say there are two homes in a neighborhood, one is small and only $100,000 and the other is big and $200,000. Now pretend that you buy the small starter home for $100,000. In a few years your property values double.

You are super happy because you now have $100,000 in equity! You’re rich! Time to upgrade and get the big house you really want. Only it isn’t $200,000 anymore. It’s value also doubled and is now $400,000!

You use your $100,000 capital gain, but you are still left paying $300,000 for the bigger house, when before the property values doubled you could have bought it for only $200,000. In addition to that, all of your closing fees, commissions and taxes will be way more thanks to the new property value. Bottomline, property values go up and you pay more!

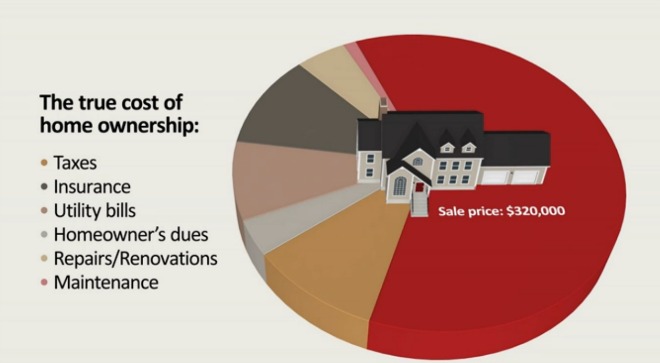

7. It All Adds UP:

There are many costs of homeownership that people forget or are simply unaware of.

Homeowners insurance is about 1,000 a year; Homeowner Association dues vary, but average about $1,000 a year; property tax is about 1.25% of the home’s market value, so on a $200,000 that is $2,500 a year; PMI or Primary Mortgage Insurance with around 1%, or $2,000 on your $200,000; and of course, there is maintenance which runs about 3% a year, or $6,000 on a $200,000 home.

That’s $10,500 a year for a home worth $200,000! 50 years of homeownership means you will spend $525,000 in fees and costs most people don’t even consider when they buy a home.

Now, I’m not saying that you shouldn’t buy a home. I think you should, but understand how the system is loaded against you, and then navigate accordingly.

Now, I’m not saying that you shouldn’t buy a home. I think you should, but understand how the system is loaded against you, and then navigate accordingly.

If you can, pay cash. You may not be able to afford your dream home right away, but with the money you save, you soon will!

At some point in the future, I will offer some tips on how get the most from your family home purchase. If you have any questions or comments, leave them below!

Love this! We are also the “lucky” owners– ahem, long-time renters– of 2 homes. One has been rented out (which barely pays for itself, let alone for any repairs) and the other we have lived in. And after 10 years of “home ownership” during the last 5 we have finally learned a lot about finances. Now, if someone is thinking about buying, I’m not nearly as positive about it as I used to be, especially because so many people get way too big of a debt buying a house!

My uncle joked that my husband and I must be rich since we own 2 houses. I replied that we are just doubly in debt!

We actually just moved back into the rental and are trying to sell the bigger home, in the hopes of someday getting out of this mortgage debt! I sure wish we had understood this all better 10 years ago!

Jamie @ Coffee With Us 3 recently posted…Pretty Pintastic Party #49

That’s all well and good but finding a rental property for a family of 9 when your landlord sells your house out from under you after 9 years is no picnic. Average mortgage payments in our area are much lower then average rents for similar properties. In addition if we were buying a home we could put our family of 9 in a smaller home then we can while renting. No one wants to rent a 3 bedroom to our family but we could buy one and no one would care. Between that and the price difference between monthly rent and typical mortgage payments we would cut our housing costs and gain stability for our kids.

Yes, there is certainly a time to buy, but it is still good to know all the “hidden” costs before you do. I hope that you can find a great home for your family.

The banks served the unknowing public a slice that was too big to chew – predatory lending fooled people into thinking they could get that, for only this…like you said, miseducated. However, when most people we’re getting booted I slid in at a nice low 3.25% apr – and the way rents are in my area, my mortgage is a steal and when I’m ready I can get double my mortgage if I rent this place out. So in summary, you just have to stay within your means.

chris rubenstein recently posted…How to Install a Smoke Detector the Right Way – So It Works!

Yes, there are certainly good times to buy. The last house that I bought was a great investment! It is just important to know all the costs before jump into one.

I deal in real estate but I always prefer to go with property appraisers who really help me to take right decision as they have depth in knowledge about the real cost of the property.

What kind of credit score do you need to buy a house?

Just a quick note to tell you that I have a passion for the topic “real estate” at hand. I am going to share the post on my social media pages to see my friends and followers.

Thanks for the share!

I deal in real estate; however, I usually choose to go together with assets appraisers who help me to make the proper selection as they have got intensity in know-how approximately the actual price of the property.

This article sheds light on the sad truth about homeownership, providing a realistic perspective on the challenges and potential downsides. It’s important to have a balanced understanding of homeownership, including the financial commitments, maintenance responsibilities, and potential limitations. This article encourages readers to critically evaluate their personal circumstances and consider alternative housing options that may better suit their lifestyle and financial goals. It’s a thought-provoking piece that prompts meaningful discussions about the pros and cons of homeownership.